In the complex world of global finance, there is one invisible force that acts as the ultimate “gravity” for asset prices: interest rates. Whether you are a casual investor with a few shares of a tech giant or a seasoned professional managing a multi-million dollar portfolio, the decisions made by central banks—specifically the Federal Reserve in the United States—dictate the rhythm of the market.

Understanding the relationship between interest rates and the stock market is arguably the most important piece of financial literacy you can acquire. When interest rates move, they send ripples through corporate boardrooms, consumer bank accounts, and trading floors across the globe.

In this guide, we will peel back the layers of monetary policy to explain exactly why a small percentage change in a central bank’s rate can cause a trillion-dollar swing in market capitalization.

1. The Cost of Capital: How Higher Rates Squeeze Corporate Profits

The most direct way interest rates affect the stock market is through the cost of borrowing. Most modern corporations do not operate solely on the cash they have in the bank; they use debt to fund expansions, buy back shares, or manage daily operations.

The Impact on the Bottom Line

When a central bank raises interest rate targets, banks follow suit by increasing the rates they charge on business loans and lines of credit.

-

Higher Interest Expense: For companies with significant debt, an increase in rates leads to higher interest payments. These payments are deducted from the company’s revenue, directly reducing the Net Income (profit).

-

Reduced Expansion: When borrowing becomes expensive, companies are less likely to build new factories, hire more staff, or invest in Research and Development (R&D). This slowdown in growth typically leads to lower stock prices as investors adjust their expectations for the company’s future.

2. The Discounted Cash Flow (DCF) Effect: Why Valuations Fall

For many laypeople, it is confusing why a profitable tech company’s stock might crash even if its business is doing well, simply because interest rates rose. The answer lies in the mathematical models used by professional analysts to value companies, primarily the Discounted Cash Flow (DCF) analysis.

The Mathematical “Gravity”

The value of a stock today is essentially the sum of all the money it will make in the future, brought back to “today’s dollars.” To calculate this, analysts use a discount rate, which is heavily influenced by current interest rates.

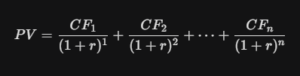

The formula for the Present Value (PV) of a future cash flow (CF) looks like this:

Where:

-

CF = Cash Flow in a given year.

-

r = The discount rate (interest rate).

-

n = The number of years.

The Logic: As the value of r (interest rate) increases, the denominator of the fraction becomes larger. This makes the Present Value smaller. Consequently, when rates rise, the “value” of a company’s future earnings drops, leading to a lower stock price today.

3. The Competition for Capital: Stocks vs. Bonds

Investors are always looking for the best return for the least amount of risk. This is often referred to as the Equity Risk Premium.

Risk-Free Returns

Government bonds (Treasuries) are often considered “risk-free” because they are backed by the government’s ability to print money or tax citizens.

-

When rates are low (e.g., 1%): Investors find bonds boring. They “flee” to the stock market to find better returns, driving stock prices up.

-

When rates are high (e.g., 5%): A 5% guaranteed return from a government bond looks very attractive compared to the volatile stock market. Many investors sell their stocks and move their money into bonds or high-yield savings accounts.

This massive shift in capital—moving from “risk-on” assets (stocks) to “risk-off” assets (bonds)—is a primary driver of market sell-offs during rate-hike cycles.

4. Consumer Spending Power: The Trickle-Down Effect on Earnings

The stock market is a reflection of the economy, and the economy is driven by consumer spending. Interest rates act as a valve that controls how much “extra” money consumers have in their pockets.

Mortgages, Auto Loans, and Credit Cards

When interest rates rise:

-

Mortgages: Monthly payments for new home buyers increase, cooling the housing market.

-

Auto Loans: Buying a car becomes more expensive, leading to fewer sales for manufacturers.

-

Credit Cards: Variable interest rates on credit cards rise, leaving consumers with less disposable income to spend on “discretionary” items like iPhones, vacations, or dining out.

When consumers spend less, companies earn less revenue. When revenue falls, stock prices follow. This is why retail and consumer-facing stocks are often the first to feel the pain of a “hawkish” Federal Reserve.

5. Winners and Losers: Which Sectors Are Most Sensitive?

Not all stocks react the same way to interest rate changes. Understanding the “Sector Sensitivity” can help you protect your portfolio.

The Losers: Growth and Technology

Growth stocks, especially in the Tech sector, often trade at high valuations based on profits they expect to make 10 or 20 years from now. As we saw in the DCF formula, those far-future profits are the most sensitive to high interest rates. This is why the Nasdaq often falls further than the Dow Jones when rates rise.

The Losers: Real Estate and Utilities

Sectors like Real Estate (REITs) and Utilities are capital-intensive and carry a lot of debt. They also pay high dividends. When bond yields rise, these “income-generating” stocks lose their appeal, and their high debt becomes more expensive to service.

The Winners: The Financial Sector

Banks and insurance companies often benefit from moderately rising interest rates. Banks can increase the “spread” between what they pay savers and what they charge borrowers (the Net Interest Margin). When rates rise, banks typically become more profitable, assuming the economy doesn’t crash into a recession.

6. The Fed Pivot and Market Psychology

The stock market doesn’t just react to what the interest rate is today; it reacts to what it thinks the rate will be tomorrow. This is known as Forward Guidance.

Anticipation vs. Reality

If the market expects the Fed to raise rates by 0.50% but they only raise them by 0.25%, the stock market might actually rally on the news. This is because the “news” was better than expected.

The most anticipated event in finance is the “Fed Pivot.” This occurs when the central bank stops raising rates and prepares to start cutting them. A pivot signal is often the catalyst for the start of a “Bull Market,” as investors begin pricing in cheaper borrowing and higher future valuations.

7. Global Currency Fluctuations and International Trade

For investors in the United States or those holding U.S. stocks, interest rates have a significant impact on the U.S. Dollar (USD).

The Strong Dollar Effect

Higher interest rates in the U.S. attract foreign investors who want to earn that higher yield. To buy U.S. bonds, they must first buy U.S. dollars. This increases the demand for the dollar, making it “stronger” compared to the Euro or Yen.

-

Bad for Multinationals: Companies like Coca-Cola or Microsoft that sell products globally find that their international earnings are worth less when converted back into a “strong” dollar.

-

Cheaper Imports: Conversely, a strong dollar makes it cheaper for U.S. companies to import goods from abroad, which can help lower production costs.

8. Checklist for Investors

As you navigate a changing interest rate environment, keep this checklist in mind:

| Rate Environment | Market Sentiment | Best Strategies |

| Rising Rates | Bearish/Cautionary | Focus on “Value” stocks, Cash-rich companies, and Financials. |

| Stable/High Rates | Neutral | Focus on quality earnings and defensive sectors (Healthcare/Consumables). |

| Falling Rates | Bullish/Aggressive | Focus on Growth, Tech, and Real Estate. |

| Low/Zero Rates | High Speculation | Broad market index funds and high-growth equities. |

Mastering the Invisible Thread

Interest rates are the invisible thread that connects every corner of the financial world. While a rising rate environment can be painful for stock prices in the short term, it is often a sign that the economy is strong enough to handle it.

As an investor, your goal shouldn’t be to “predict” the next Fed move, but to build a portfolio that is resilient regardless of where the “gravity” of interest rates sits. By understanding the math of valuations, the competition between stocks and bonds, and the impact on corporate debt, you can remain calm while others panic, looking for opportunities in the volatility.