In the world of personal finance, few concepts are as celebrated yet as misunderstood as compound interest. Albert Einstein famously referred to it as the “Eighth Wonder of the World,” stating, “He who understands it, earns it; he who doesn’t, pays it.”

But what exactly is compound interest, and how does it transform a modest savings account into a significant wealth-building engine? Whether you are saving for retirement, a child’s education, or financial independence, understanding the mechanics of compounding is the single most important step you can take toward your goals.

What is Compound Interest? Understanding the Core Mechanism

At its most basic level, compound interest is interest calculated on the initial principal, which also includes all the accumulated interest from previous periods. To understand this, we must first look at its simpler counterpart: Simple Interest. Simple interest is only paid on the original amount of money you deposited (the principal). If you invest $1,000 at a 10% simple interest rate, you earn $100 every year. After 10 years, you have $2,000.

Compound interest, however, creates a “snowball effect.” In the first year, you earn 10% on your $1,000 ($100). In the second year, you earn 10% on your new balance of $1,100 ($110). By the tenth year, you aren’t just earning interest on your original thousand; you are earning interest on the interest that has been piling up for a decade.

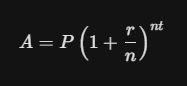

The Mathematical Engine: Breaking Down the Compound Interest Formula

While you don’t need to be a math genius to benefit from compounding, understanding the formula helps you see which “levers” you can pull to accelerate your wealth.

The standard formula for annual compounding is:

Where:

-

A = the future value of the investment/loan, including interest.

-

P = the principal investment amount (the initial deposit).

-

r = the annual interest rate (decimal).

-

n = the number of times that interest is compounded per unit t.

-

t = the time the money is invested or borrowed for.

The Three Pillars of the Formula

-

Principal (P): The more you start with, the larger the base for interest to grow.

-

Rate (r): Even a 1% difference in your interest rate or investment return can result in hundreds of thousands of dollars in difference over 30 years.

-

Time (t): This is the most powerful variable. Because t is an exponent, it has a disproportionate impact on the final result.

Why Time is Your Greatest Asset in Wealth Building

Many people wait until they have a “significant” amount of money to start investing. This is one of the costliest mistakes in finance. In the world of compounding, time is more important than the amount of money you contribute.

Consider two investors, Investor A and Investor B:

-

Investor A starts at age 25. They invest $500 a month for 10 years and then stop entirely at age 35, leaving the money to grow at a 7% annual return.

-

Investor B waits until age 35 to start. They invest the same $500 a month, but they do it for 30 years until they turn 65, also at a 7% return.

Even though Investor B contributed three times as much money over a much longer period, Investor A still ends up with more money at age 65. This is because Investor A’s money had an extra decade to compound quietly in the background.

The Rule of 72: A Shortcut for Savvy Investors

If you want to quickly estimate how long it will take for your money to double, use the Rule of 72. It’s a simple mental math trick used by financial pros.

How it works: Divide 72 by your expected annual rate of return. The result is the approximate number of years it will take for your initial investment to double.

-

At a 6% return, your money doubles in 12 years ($72 / 6$).

-

At a 10% return, your money doubles in about 7.2 years ($72 / 10$).

-

At a 12% return, your money doubles in just 6 years ($72 / 12$).

This rule highlights why seeking slightly higher returns (within your risk tolerance) and giving your investments time to double multiple times is the key to becoming a millionaire.

How Compounding Frequency Changes Your Final Balance

The formula mentioned earlier includes a variable ($n$) for compounding frequency. Interest can be compounded annually, semi-annually, quarterly, monthly, or even daily.

The more frequently interest is compounded, the faster your balance grows. While the difference between monthly and daily compounding might seem like pennies on a small account, it becomes substantial on larger balances over long periods.

For example, a $100,000 investment at 5% interest:

-

Compounded Annually: $105,000.00 after one year.

-

Compounded Monthly: $105,116.19 after one year.

-

Compounded Daily: $105,126.75 after one year.

When choosing a high-yield savings account or a certificate of deposit (CD), always look for APY (Annual Percentage Yield) rather than just the “interest rate.” APY takes the compounding frequency into account, giving you a true apples-to-apples comparison.

Best Investment Vehicles to Harness Compound Interest

Not all financial products are created equal when it comes to compounding. To truly maximize the effect, you need assets that offer growth and the ability to reinvest earnings.

1. Dividend Reinvestment Plans (DRIPs)

When you own stocks that pay dividends, you have two choices: take the cash or reinvest it. By using a DRIP, you automatically use your dividends to buy more shares of the stock. This increases the number of shares you own, which increases your next dividend payment, creating a powerful cycle of compounding.

2. Index Funds and ETFs

Broad market index funds (like those tracking the S&P 500) are excellent for compounding. As the companies within the index grow in value and pay dividends, the overall value of your holding compounds. Over the last century, the US stock market has returned an average of about 10% annually before inflation.

3. Retirement Accounts (401k and IRA)

These are the “secret weapons” of compounding. In a standard brokerage account, you owe taxes on dividends and capital gains every year, which “leaks” money out of your compounding engine. In a Roth IRA or 401(k), your money grows tax-free or tax-deferred, allowing every single cent to stay invested and compound.

4. High-Yield Savings Accounts (HYSA)

For short-term goals or emergency funds, HYSAs offer a safe way to compound cash. While the returns are lower than the stock market, the compounding is often monthly, and the risk to your principal is virtually zero.

The Stealth Killers: Fees, Taxes, and Inflation

Compounding is a double-edged sword. Just as it can build wealth, certain factors can “compound” in the opposite direction, eating away at your future fortune.

The Impact of Investment Fees

A 1% management fee might sound small, but over 30 years, it can cost you hundreds of thousands of dollars. Why? Because that 1% isn’t just “gone”—the future growth of that 1% is also gone. High-fee mutual funds are the enemies of compounding; this is why many experts recommend low-cost index funds.

The Erosion of Inflation

If your investment earns 5% but inflation is 3%, your “real” rate of return is only 2%. To truly build wealth, your compounding rate must significantly outpace the rising cost of living.

Tax Drag

If you have to pay 20% in taxes on your gains every year, you are significantly slowing down your snowball. Utilizing tax-advantaged accounts is like removing a speed limit from your wealth accumulation.

The Dark Side: How Compound Interest Works Against You in Debt

It is vital to remember that compound interest works exactly the same way on debt. This is why credit cards are so dangerous.

Most credit cards compound interest daily. If you carry a balance, you are paying interest on the interest from yesterday. At a 20% or 25% APR, the “snowball” works against you with terrifying speed. While it might take 7–10 years to double your money in the stock market, a credit card debt can double in less than 4 years if only minimum payments are made.

Strategy: Always pay off high-interest debt before focusing heavily on investing. You cannot “out-invest” a 25% interest rate.

Psychological Hurdles: Why Most People Fail at Compounding

The biggest challenge with compound interest isn’t the math—it’s patience.

In the beginning, the growth is boring. If you invest $10,000 and earn 7%, you only have $10,700 after a year. It doesn’t feel life-changing. You might be tempted to pull the money out to buy a new car or try a “hot” new crypto coin.

However, the “Magic” happens in the later years. In a 30-year investment horizon, more than half of your total wealth is often generated in the final five to seven years. Compounding requires a “set it and forget it” mentality. Those who jump in and out of the market to “time” the cycles often interrupt the compounding process, resetting their clock and losing out on the most explosive growth phases.

Steps to Maximize Your Compounding Potential

To make the most of this financial phenomenon, follow these four pillars:

-

Start Today: Even a small amount invested now is worth more than a large amount invested ten years from now.

-

Reinvest Everything: Don’t spend your dividends or interest. Turn on automatic reinvestment.

-

Minimize Leakage: Keep fees low by using low-cost ETFs and keep taxes low by using IRAs or 401(k)s.

-

Be Patient: Ignore the daily noise of the news. Let the math do the heavy lifting over decades, not days.

Compound interest is the bridge between working for your money and having your money work for you. By understanding these principles and staying disciplined, financial freedom isn’t just a possibility—it’s a mathematical certainty.