When you are in your 20s or early 30s, your financial priorities are usually focused on the “now.” You are likely navigating the start of your career, managing student loan debt, perhaps saving for a first home, or wondering how to build an emergency fund. In this stage of life, the idea of a life insurance policy—something traditionally associated with older age and mortality—can feel irrelevant.

However, from a purely financial and strategic perspective, your youth is actually your most powerful asset in the insurance market. In the United States, life insurance is priced primarily on risk, and as a young person, your risk profile is at its lowest.

In this guide, we will break down the economics of early life insurance, explain why the “death benefit” is only one part of the story, and help you determine if buying a policy today is a savvy investment or an unnecessary expense.

The Cost of Waiting: How Age and Health Impact Premiums

The most compelling argument for buying life insurance while young is the cost. Life insurance premiums are determined by “actuarial tables”—mathematical models that predict life expectancy.

The “Youth Discount”

When you apply for a policy at age 25, the insurance company assumes you have decades of premium-paying years ahead of you. Consequently, they offer you significantly lower rates than they would to someone aged 45 or 55.

By purchasing a policy early, particularly a “Level Term” policy, you can lock in these low rates for 20 or 30 years. This means you could be paying the same “healthy 25-year-old” price when you are 50, whereas your peers who waited will be paying triple or quadruple for the same amount of coverage.

Protecting Your Co-Signers: The Student Loan Trap

A common misconception is that life insurance is only necessary if you have children or a spouse. However, for many young Americans, the biggest financial risk is their debt.

Federal vs. Private Student Loans

-

Federal Loans: Usually, federal student loans are discharged (forgiven) if the borrower passes away.

-

Private Student Loans: These are a different story. Many private lenders do not forgive the debt upon death. If your parents or a relative co-signed your private student loans, they would be legally responsible for the balance if something happened to you.

A small life insurance policy ensures that your loved ones aren’t left with a $50,000 or $100,000 debt burden that they never expected to pay.

The Insurability Risk: Why Buying Now Protects Your Future

One of the most overlooked benefits of early life insurance is the concept of Insurability. Right now, you are likely at your healthiest. But as we age, we develop “pre-existing conditions”—high blood pressure, high cholesterol, diabetes, or even a history of anxiety or depression.

Securing the “Right to Insure”

If you develop a chronic health condition at age 32, you might find it difficult or prohibitively expensive to get a life insurance policy later when you have a family. By buying a policy while you are young and healthy, you ensure you have coverage in place regardless of what happens to your health in the future.

Many young people opt for a Guaranteed Insurability Rider. This allows you to increase your coverage at specific intervals (like when you get married or have a child) without undergoing a new medical exam.

Term vs. Whole Life: Which Path Fits the Young Professional?

If you decide to move forward, you must choose between the two primary “flavors” of life insurance. Each has a drastically different impact on your finances.

Term Life Insurance: The Budget-Friendly Choice

Term insurance provides coverage for a set period (usually 10, 20, or 30 years). It is pure protection with no “investment” component.

-

Pros: Extremely affordable. A healthy 25-year-old can often get $500,000 in coverage for the price of a few cups of coffee per month.

-

Cons: If you outlive the term, the coverage ends and you get no money back.

Whole Life Insurance: The Wealth-Building Tool

Whole life is “permanent” insurance that lasts as long as you pay the premiums. It also includes a Cash Value component that grows over time.

-

Pros: It acts as a “forced savings” account. You can borrow against the cash value for a down payment on a house or for business capital.

-

Cons: Much more expensive—often 10 to 15 times the cost of term insurance.

Life Insurance as a “Living Benefit”: More Than a Death Payout

Modern life insurance policies in the US often include Living Benefit Riders. These allow you to access your death benefit while you are still alive under certain circumstances.

-

Critical Illness: If you are diagnosed with a covered illness (like cancer or a heart attack) but survive, the policy may pay out a lump sum to help with medical bills or lost wages.

-

Chronic Illness: If you can no longer perform daily activities (like eating or bathing), the policy can provide funds for long-term care.

-

Terminal Illness: If you are diagnosed with a terminal condition, you can access the funds to enjoy your remaining time or handle end-of-life expenses.

For a young person, these “living benefits” act as a supplement to disability insurance, providing a broader safety net.

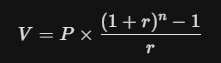

Understanding the Math: The Power of Compounding Cash Value

If you choose a permanent policy (like Whole Life or Universal Life) while you are young, you have the greatest advantage in the world: Time.

The cash value inside these policies grows tax-deferred. Using the power of compounding, the small amounts you put in during your 20s have decades to grow.

Let $V$ be the future value of the cash component, $P$ be the periodic payment, $r$ be the rate of return, and $n$ be the number of periods. The formula for the future value of an ordinary annuity illustrates why starting early matters:

When $n$ (time) is 40 years instead of 10 years, the growth is exponential. This is why many high-net-worth individuals started their “infinite banking” strategies or cash-value policies when they were just starting their careers.

The Employer-Provided Policy: Why It’s Usually Not Enough

Many young professionals feel they are “covered” because their employer provides a life insurance policy (usually equal to 1x their annual salary). While this is a great perk, it is rarely sufficient.

-

Portability: If you leave your job or are laid off, you usually lose that coverage. You are left without insurance exactly when your life is in transition.

-

Coverage Gap: If you earn $60,000, a $60,000 payout might cover a funeral and a few months of bills, but it won’t provide long-term security for a partner or pay off a mortgage.

-

No Control: You cannot customize the riders or the terms of a group policy.

Having your own private policy ensures that your protection is independent of your employment status.

Is It Better to “Buy Term and Invest the Difference”?

A popular philosophy in the personal finance world is to avoid expensive whole life policies, buy cheap term insurance, and invest the extra money in a low-cost index fund (like the S&P 500).

The Case for “Buy Term”

For most young people, this is the mathematically superior strategy. If you save $100 a month by choosing term over whole life and invest that $100 in a brokerage account, you will likely have a much larger “nest egg” after 30 years than the cash value of an insurance policy would provide.

The Case for Permanent Insurance

The only reason to choose the more expensive permanent route while young is if you have already maxed out your 401(k) and IRA and are looking for a tax-advantaged place to put extra money, or if you have a lifelong dependent (such as a child with special needs).

Common Myths About Young Adults and Life Insurance

To make a clear decision, we must debunk a few persistent myths:

-

“I don’t have dependents, so I don’t need it.” You have “future you” as a dependent. Buying now locks in the low rate that “future you” (with kids and a mortgage) will be grateful for.

-

“Life insurance is a scam.” It is a highly regulated financial contract. While some agents push high-commission products, the underlying value of risk management is a cornerstone of a solid financial plan.

-

“It’s too expensive.” For the price of a monthly Netflix subscription, most 20-somethings can secure a substantial term life policy.

How to Determine Your Coverage Needs: The DIME Formula

If you decide that life insurance is worth it, how much should you buy? Many experts suggest using the DIME Formula to calculate your “number.”

-

Debt: Total all your debt (student loans, credit cards, car loans).

-

Income: Multiply your annual salary by the number of years you want to provide for (e.g., 10 years).

-

Mortgage: The remaining balance on your home.

-

Education: The estimated cost of tuition for your current or future children.

Subtract any existing savings or assets, and that final number is the amount of coverage you should aim for.

Final Verdict

Does life insurance worth it if you are young? The answer is a resounding yes, provided you choose the right product.

For the vast majority of young adults, a 20 or 30-year Term Life policy is a brilliant move. It is an inexpensive way to hedge against the “what ifs” of life while protecting your family and your co-signers. It also guarantees that you have the “right to insure” yourself later in life when the stakes are much higher.

Don’t view life insurance as a bet on your death; view it as a strategic move to lock in a low-cost financial foundation while your health and age are at their peak.