Starting your investment journey is one of the most significant financial decisions you will ever make. However, before you can buy your first share of an AI powerhouse or a steady dividend-paying giant, you need a “gateway” to the financial markets. That gateway is your brokerage account.

In 2026, the landscape of online brokerages has evolved into a hyper-competitive arena. With the death of trading commissions and the rise of mobile-first platforms, the challenge for a beginner isn’t finding a place to invest—it’s finding the right place that aligns with your goals, protects your capital, and provides the tools you need to grow from a novice to a seasoned pro.

In this guide, we will break down every factor you must consider when choosing a brokerage, the hidden costs to watch out for, and a comparison of the top platforms currently dominating the market.

Understanding the Role of a Modern Stock Broker

At its core, a broker is an intermediary. They connect you, the investor, with the stock exchanges (like the NYSE or Nasdaq) where securities are bought and sold.

Historically, brokers were people you called on the phone who charged $50 or more per trade. Today, your broker is likely an app on your phone or a sophisticated web portal. In 2026, the role of the broker has expanded. They are now your primary source for:

-

Market Data: Real-time price quotes and financial news.

-

Custody: Safekeeping your assets and cash.

-

Tax Reporting: Providing the documents you need for the IRS or your local tax authority.

-

Education: Tutorials, webinars, and research reports to help you understand what you are buying.

The “Zero Commission” Myth: How Brokerages Actually Make Money

If you aren’t paying a $5 commission to buy a stock, how does the brokerage stay in business? Understanding this is crucial for beginners because it reveals the “hidden” incentives of the platform.

1. Payment for Order Flow (PFOF)

Many “free” brokerages don’t send your order directly to the stock exchange. Instead, they send it to a market maker (a high-frequency trading firm). The market maker pays the broker a small fee for this “order flow.” While this keeps commissions at zero, it can sometimes result in a slightly worse execution price for you—though for most long-term beginners, the difference is measured in fractions of a cent.

2. Interest on Cash Balances

When you have uninvested cash sitting in your brokerage account, the broker often moves that money into interest-bearing accounts. They keep a large portion of that interest and pass a small amount (if any) to you.

3. Securities Lending

Some brokers “lend” your stocks to short-sellers. They collect interest on these loans, which provides another revenue stream that allows them to offer you a free platform.

4. Premium Tiers and Margin Interest

Many platforms offer “Gold” or “Pro” memberships for a monthly fee. Additionally, if you borrow money from the broker to buy more stocks (investing on margin), you will pay interest on that loan.

Essential Features for the First-Time Investor

When you are just starting, you don’t need a high-speed terminal or complex option-chain analysis tools. You need a platform that makes the basics easy.

Fractional Shares: Why Entry Cost Is No Longer a Barrier

In the past, if a stock cost $3,000 per share and you only had $500, you simply couldn’t buy it. In 2026, fractional shares are a non-negotiable feature for a beginner’s brokerage. This allows you to buy $5 worth of any stock, regardless of the share price. This is essential for building a diversified portfolio with a small amount of capital.

Robust Mobile and Web Experience

You should be able to check your portfolio, research a company, and execute a trade seamlessly across all devices. A buggy app or a cluttered interface can lead to expensive mistakes, such as accidentally clicking “sell” instead of “buy.”

Customer Support Availability

As a beginner, you will have questions. Whether it’s about a tax form or a weird ticker symbol change, you need access to human support. Look for brokerages that offer 24/7 chat support or, better yet, a reliable phone line. Avoid platforms that only offer an automated “FAQ” bot for customer service.

Brokerage Account Types: Taxable vs. Tax-Advantaged IRAs

One of the most common mistakes beginners make is opening the wrong type of account. Choosing the right “container” for your investments can save you thousands in taxes.

| Account Type | Tax Treatment | Best For… |

| Standard Brokerage | Taxed on dividends and capital gains annually. | Short-term goals (under 5 years) and liquidity. |

| Traditional IRA | Contributions may be tax-deductible; taxed upon withdrawal. | Lowering your current taxable income. |

| Roth IRA | Contributions are after-tax; withdrawals in retirement are tax-free. | Long-term wealth building and tax-free growth. |

| 401(k) / 403(b) | Often includes employer matching. | Retirement and “free money” from employers. |

Security and Regulation: Keeping Your Money Safe with SIPC

You are trusting a brokerage with your hard-earned money. What happens if the brokerage goes bankrupt? This is where regulation and insurance come in.

SIPC Insurance

In the United States, your brokerage should be a member of the Securities Investor Protection Corporation (SIPC). If a member brokerage fails, the SIPC protects the securities and cash in your account up to $500,000, including a $250,000 limit for cash.

FINRA Oversight

The Financial Industry Regulatory Authority (FINRA) is a non-profit organization authorized by Congress to protect investors by ensuring the broker-dealer industry operates fairly and honestly. Always verify that your chosen broker is FINRA-registered.

Two-Factor Authentication (2FA)

In 2026, cyber threats are more sophisticated than ever. Your brokerage should offer robust security features, including biometric login and hardware-key support (like YubiKey) or app-based 2FA. Avoid any broker that only offers SMS-based 2FA, as this is vulnerable to SIM-swapping attacks.

User Interface and Educational Resources: The Hidden Value

A great brokerage for beginners should act like a teacher. Many modern platforms now include “learn” tabs that explain basic concepts like:

-

What is a P/E ratio?

-

How do dividends work?

-

The difference between a “Market Order” and a “Limit Order.”

If you find yourself constantly leaving the brokerage app to Google what a button does, that platform might not be optimized for beginners. Look for “In-app research” that provides third-party analyst ratings (like Morningstar or S&P Global) so you can get an objective view of a stock without leaving the platform.

Comparing the Giants: A Review of Top Brokerages in 2026

To help you decide, let’s look at the “Big Four” that currently lead the market for beginner investors.

1. Fidelity Investments: The All-Rounder

Fidelity is often cited as the best overall choice for beginners. They offer fractional shares (called “Stocks by the Slice”), zero account minimums, and an incredibly deep library of educational content. Their customer service is top-tier, and they offer a wide range of account types, including HSAs and IRAs.

2. Charles Schwab: The Customer Service King

Schwab is known for its “Schwab Stock Slices” and its legendary customer support. They also offer the Schwab Intelligent Portfolios, which is a robo-advisor that builds and manages a portfolio for you for $0 management fees (though it does hold a required amount of cash).

3. Vanguard: The Low-Cost Indexer

Vanguard is unique because it is owned by its funds, which are owned by the investors. It is the best place for someone who wants to buy Index Funds and ETFs and hold them for 30 years. Their interface is more traditional and less “flashy,” which can actually be a benefit for those who want to avoid the temptation of day-trading.

4. Robinhood: The Mobile Pioneer

Robinhood changed the world by making investing feel like a social media app. It is the most intuitive app on the market and perfect for someone starting with very small amounts of money. However, it lacks the deep research tools and some of the retirement account options found at Fidelity or Schwab.

Questions to Ask Before Opening Your Account

Before you hit the “Sign Up” button, go through this checklist:

-

Do they support fractional shares? (Vital for small budgets).

-

Is there an account maintenance fee? (You want $0).

-

What is the interest rate on uninvested cash? (High-yield is a bonus).

-

Are dividends automatically reinvested (DRIP)? (Crucial for compounding).

-

Do they offer the specific account type I need? (e.g., Roth IRA).

The Step-By-Step Process of Opening Your First Brokerage Account

Opening an account is now as easy as opening a bank account. It typically takes less than 10 minutes.

Step 1: Provide Personal Information

You will need your Social Security Number (or equivalent tax ID), home address, and employment information. This is required by “Know Your Customer” (KYC) laws to prevent money laundering.

Step 2: Choose Your Account Type

Select between an Individual Brokerage account (taxable) or a Retirement account (IRA).

Step 3: Link Your Bank Account

You can usually do this via a service like Plaid, allowing for instant transfers.

Step 4: Set Up a Recurring Deposit

The most successful beginners don’t wait for a “good time” to invest. They set up an automatic transfer of $50 or $100 every payday.

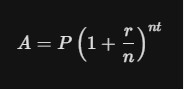

The math behind this is the power of compounding:

Where:

-

A is the final amount.

-

P is the principal (your initial investment).

-

r is the annual interest rate.

-

n is the number of times interest is compounded per year.

-

t is the number of years.

Avoiding Common Beginner Mistakes with Your New Brokerage

Once you have your account open, the real challenge begins: not getting in your own way.

Avoid “Over-Trading”

Because it is so easy to buy and sell on a smartphone, many beginners trade too often. Every time you sell a stock for a profit in a taxable account, you trigger a tax bill. In 2026, the best strategy remains “Buy and Hold.”

Don’t Ignore the “Expense Ratio”

When buying ETFs, pay attention to the expense ratio. This is the annual fee the fund manager takes. A fee of 0.03% is great; a fee of 0.75% is expensive and will eat your gains over decades.

Market Orders vs. Limit Orders

In a volatile market, never use a “Market Order.” This tells the broker to buy at any price. Instead, use a Limit Order, where you specify the maximum price you are willing to pay. This protects you from sudden price spikes.

Taking the First Step in 2026

Choosing a brokerage is like choosing a pair of hiking boots. It doesn’t matter how expensive they are if they don’t fit your feet.

If you want a simple, mobile-first experience to buy a few shares of your favorite companies, a platform like Robinhood is excellent. If you are building a multi-generational retirement nest egg and want deep research and world-class support, Fidelity or Schwab are the industry standards.

The most important thing to remember is that you can always change later. Most brokerages offer an “ACATS” transfer, which allows you to move your entire portfolio from one broker to another without selling your stocks.

Don’t let “analysis paralysis” stop you. Pick a reputable, SIPC-insured broker today, set up a small recurring deposit, and start letting the power of the global economy work for you.