Applying for a loan can be a nerve-wracking experience. Whether you are trying to buy your first home, finance a reliable vehicle, or secure a personal loan to consolidate high-interest debt, waiting for the lender’s decision is always stressful. When that notification finally arrives, discovering that your loan application was denied can feel like a devastating personal and financial blow.

However, it is vital to understand that a loan rejection is not a permanent label on your financial future. It is simply a structural sign from a lender’s mathematical risk algorithm indicating that your current financial profile does not match their specific underwriting criteria today.

Lenders are not making emotional choices; they are running math equations designed to protect their capital. If you can decode exactly why your application fell short, you can systematically patch the vulnerabilities in your financial record, optimize your profile, and reapply with a much higher probability of securing an approval.

Why Banks Reject Financing Requests: Demystifying the Automated Underwriting Process

In the modern financial landscape, initial loan processing is rarely managed entirely by human eyes. Instead, banks, credit unions, and online fintech platforms rely heavily on complex algorithms known as Automated Underwriting Systems (AUS).

When you click “submit” on an application form, the software instantly aggregates data from your credit reports, public records, and financial statements, evaluating your file against thousands of predetermined risk triggers.

[User Application Submitted]

│

▼

[Automated Underwriting System (AUS)] ───► Evaluates Credit, DTI, & Collateral

│

├───► Passed Thresholds ───► [Human Loan Officer Review] ───► Approved!

│

└───► Risk Trigger Hit ───► [Automated System Rejection] ───► Denied

If your financial history triggers a high-risk flag—such as a debt ratio that is a fraction too high or a credit score that sits one point below their absolute minimum cutoff—the system will issue an automated rejection.

To override these automated denials, you must understand the primary foundational metrics that lenders look at when scoring your risk profile.

High Debt-to-Income (DTI) Ratios: The Number One Reason for Loan Application Denials

Even if you maintain a perfect credit history and earn a comfortable six-figure salary, a high Debt-to-Income (DTI) ratio is the single most common reason lenders decline loan requests. Your DTI ratio measures your ability to manage your monthly payments and pay back the money you borrow.

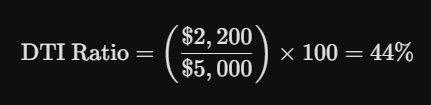

Lenders calculate your DTI by taking the total sum of all your mandatory monthly debt obligations and dividing it by your gross (pre-tax) monthly income.

The Debt-to-Income Calculation Formula:

Understanding Front-End vs. Back-End DTI Limits

For complex loans like mortgages, lenders split this metric into two distinct categories:

-

Front-End DTI Ratio: The percentage of your gross monthly income that will go strictly toward housing expenses, including the new principal, interest, property taxes, and homeowners insurance. Traditional limits usually restrict this to 28%.

-

Back-End DTI Ratio: The percentage of your income required to cover all recurring monthly liabilities combined, including minimum credit card balances, auto loans, student loans, child support, and the projected new loan payment. Traditional guidelines prefer this to stay below 36% to 43%.

A Practical Example of DTI Failure

Let’s look at how a high DTI can derail an application for an otherwise strong borrower:

| Financial Element | Monthly Value |

| Gross Monthly Income | $5,000 |

| Existing Auto Loan Payment | $450 |

| Minimum Credit Card Obligations | $200 |

| Student Loan Minimums | $350 |

| Projected New Loan Payment | $1,200 |

| Total Future Monthly Debt Burden | $2,200 |

To find this borrower’s back-end DTI ratio, we apply the formula:

If this applicant is applying for a conventional mortgage or a prime personal loan with a strict 40% maximum DTI cap, their application will be automatically rejected. Despite making good money, too much of their cash flow is already tied up in existing commitments, leaving little breathing room to handle an unexpected financial emergency.

Low Credit Scores and Subprime Credit History Profiles

Your credit score functions as your primary financial grade. It tells an underwriter how responsibly you have treated borrowed capital over the preceding years. When your baseline score drops below a lender’s risk floor, securing an approval becomes incredibly challenging.

The Most Common Credit Score Pitfalls

A low credit score rarely happens overnight. It is typically the product of specific negative events recorded in your consumer credit reports:

-

Delinquencies and Late Payments: Because your payment history makes up 35% of your total credit score calculation, even a single payment marked as 30 days late can cause a major score drop.

-

High Credit Utilization Ratios: If your credit card balances hover near your total credit limits, your utilization ratio is too high. Lenders view maxed-out credit lines as a sign that a borrower is overextended and relying on credit to cover daily living costs.

-

Active Collections and Charge-Offs: If a previous creditor gave up on collecting a debt and sold it to a collection agency, it leaves a severe scar on your record that signals a high default risk to future lenders.

-

Public Records (Bankruptcy and Judgments): Recent bankruptcies or civil judgments indicate severe financial distress, causing automated systems to reject applications until a significant amount of time has passed.

Minimum Credit Thresholds by Loan Product

Lenders look for different minimum credit standards depending on the type of financing you seek:

[Credit Score Scale]

300 ───────────────────── 580 ────────────── 620 ────────────── 660 ───────────────────── 850

│ │ │ │ │

└─── Deep Subprime ───────┴─── FHA Mortgages ┴── Auto & Personal┴── Prime Conventional ───┘

(Extreme Risk / Denied) (Govt-Backed) (Standard) (Best Terms & Rates)

If your score falls into the subprime or deep subprime categories, most prime institutions will deny your application outright rather than risk a default.

Unverifiable Income, Gap-Filled Job History, and Self-Employment Obstacles

Lenders want assurance that you possess a stable, recurring source of income that will last throughout the entire lifespan of the loan. If your source of income appears unpredictable or difficult to document, underwriters will lean toward a denial to protect their capital.

The Two-Year Employment Stability Standard

Traditional lenders heavily prefer applicants who can document a steady two-year employment history within the exact same line of work or industry. If you have cycled through four different employers in the past 12 months, or if you have large, unexplained gaps in your employment history, it raises red flags regarding your long-term income reliability.

The Self-Employment and 1099 Dilemma

Being your own boss is great for your lifestyle, but it can complicate your path to a loan approval. When a traditional W-2 employee applies for financing, proving income is easy—they simply provide a few recent pay stubs.

For self-employed business owners, independent contractors, and freelance gig workers, the verification process is much more strict:

-

The Net Income Trap: Lenders calculate your self-employed income based on the net taxable income listed on your federal tax returns, not your gross revenue. If your business brought in $100,000 last year, but your accountant wrote off $60,000 in business expenses to lower your tax liability, the lender views your actual qualifying income as only $40,000.

-

Fluctuating Monthly Cash Flows: If your business income spikes dramatically in the summer but drops to near zero in the winter, underwriters may average your income over a 24-month window or exclude erratic earnings altogether, leading to an unexpected denial.

Low Property Appraisal or Insufficient Collateral Value

Sometimes, a loan application is rejected through no fault of your own personal finances. If you are applying for an asset-backed loan—such as a mortgage or an auto loan—the property or vehicle itself serves as the collateral securing the debt. If the asset fails to pass the lender’s evaluation benchmarks, the entire deal can fall apart.

The Dynamics of Loan-to-Value (LTV) Ratios

Lenders manage their collateral risk by calculating a Loan-to-Value (LTV) ratio, which compares the total size of the loan you are requesting against the independent appraised market value of the asset.

Why a Low Appraisal Triggers a Loan Denial

Imagine you agree to purchase a home for $350,000. You plan to put down $10,000 and borrow $340,000 from the bank. However, during the underwriting process, an independent real estate appraiser evaluates the property and determines its true current market value is only $320,000.

[Purchase Agreement Price: $350,000]

│

▼

[Independent Appraisal Value: $320,000]

│

▼

[The Appraised Gap: $30,000] ───► Lender refuses to finance this deficit.

│

▼

[Borrower Outcome] ──────────────► Application Denied (Unless buyer covers gap in cash).

The lender will refuse to approve a $340,000 loan on a home that is only worth $320,000 because they would be instantly exposed to a major financial deficit if they had to repossess and sell the property. Unless you can successfully negotiate a lower purchase price with the seller or pay the $30,000 appraisal gap out of your own pocket in cash, the lender will deny the application to keep their risk balanced.

Application and Documentation Errors: The Hidden Deal-Killers

Not every loan denial stems from deep financial distress. Millions of applications are rejected each year simply due to clerical errors, incomplete verification uploads, or administrative oversight.

1. Simple Data Mismatches

If the legal name, social security number, or home address on your loan application does not align perfectly with the records held by the major credit bureaus or your tax filings, it triggers identity fraud alerts within the automated underwriting software. Rather than spending manual hours solving the puzzle, the system will often issue an immediate denial.

2. Credit File Freezes and Locks

With identity theft and data breaches on the rise, millions of consumers wisely keep a permanent credit freeze active on their files at Equifax, Experian, and TransUnion.

However, if you forget to temporarily “thaw” your credit files before clicking submit on a loan application, the lender’s automated query will receive an error message. Many systems treat a blocked credit check as an automatic rejection rather than putting the file on hold.

3. Unseasoned Cash and Untraceable Deposits

When processing a large loan, underwriters look closely at your recent bank statements to verify where your down payment cash originated.

If you recently deposited a large chunk of untraceable cash into your account—such as selling a personal item without a clear bill of sale or accepting an undocumented loan from a family member—the lender cannot legally use those funds to qualify you due to strict federal anti-money laundering regulations. If those untraceable funds are excluded, you may fall short of the required cash reserves, resulting in a denial.

What to Do If Your Loan Is Denied: A Step-by-Step Financial Recovery Roadmap

Receiving a loan denial notice is frustrating, but it also gives you a clear checklist for improvement. If you approach the situation methodically, you can convert a rejection into a successful approval on your very next attempt.

The Post-Denial Recovery Strategy

Smart Alternatives for Borrowers Struggling with Traditional Loan Approvals

If traditional commercial banks continue to deny your requests and your financial profile requires real time to rebuild, you do not necessarily have to abandon your plans. Several alternative lending structures can help bridge the gap safely:

1. Tap Into Local Credit Unions

Credit unions operate as non-profit financial cooperatives owned directly by their members. Because they lack the heavy corporate overhead of international megabanks, they feature significantly more flexible underwriting standards.

A credit union loan officer is far more likely to engage in manual underwriting—looking at your real personal story, your community standing, and your local job longevity rather than relying strictly on an automated credit score threshold.

2. Leverage a Reliable Co-Signer

If your credit score or income history cannot pass muster on its own merits, you can add a highly creditworthy family member or spouse to your loan application as a co-signer.

The co-signer assumes full legal responsibility for the loan balance if you fail to make payments. This added layer of security dramatically reduces the lender’s risk profile, helping you secure an approval and access far more competitive interest rates.

3. Consider Secured Loan Options

If you are struggling to qualify for an unsecured personal loan, consider switching to a secured loan structure. By backing the loan with a verifiable asset—such as a personal savings certificate of deposit (CD), a paid-off vehicle title, or liquid investment accounts—you give the lender a direct way to recover their capital if you default. This extra protection makes lenders much more willing to approve borrowers with thin or recovering credit files.

Key Risk Factors: A Quick Reference for Loan Applicants

To help you quickly diagnose your financial position, this table summarizes the primary reasons loan applications face rejection alongside the targeted actions needed to solve each issue.

| Core Denial Reason | Primary Underwriting Trigger | Most Effective Repair Strategy |

| Excessive DTI Ratio | Total back-end obligations exceed 43% to 50% of gross income. | Pay down revolving card balances; pay off small installment accounts; secure a co-signer. |

| Subprime Credit Score | Baseline FICO score sits below the institutional risk floor. | Audit reports for reporting errors; remove collections via disputes; pay bills on time. |

| Unverifiable Income | Net taxable income on 1099/tax returns falls below threshold. | Provide full tax histories; use bank statement loans; lower written-off business deductions. |

| Collateral Deficit | Independent asset appraisal returns lower than purchase price. | Negotiate a lower purchase price; cover the appraisal gap with cash; find an alternative asset. |

| Clerical Errors | Name, SSN, or address data mismatches fraud systems. | Thaw credit freezes before applying; double-check identity fields for accuracy. |

Frequently Asked Questions About Loan Rejections and Approval Overturns

How long should I wait to reapply after getting a loan denial?

There is no legal waiting period required before submitting a new loan application, but applying again the very next day without making changes is a recipe for another rejection. Every hard application leaves an inquiry on your report, which can lower your score slightly. It is best to wait 30 to 90 days to give yourself enough time to pay down balances, clear up errors, or build up your employment history before trying again.

Does getting denied for a loan lower my credit score?

No, the act of a lender denying your application does not impact your credit score. Credit bureaus only record the fact that an inquiry was made; they have no way of knowing whether the lender said yes or no. The minor dip in your score comes entirely from the initial hard credit inquiry generated when you submitted the paperwork.

Can a lender change their mind and overturn a loan denial?

Yes, loan denials can be reversed through a formal process called a loan reconsideration request. If you believe your application was rejected due to a data error, an incorrect credit file entry, or a temporary misunderstanding regarding your self-employment files, you can contact the lender’s underwriting department directly. By providing clear paperwork to correct the mistake, an underwriter can manually review your file and overturn the automated denial.