Albert Einstein famously called compound interest “the eighth wonder of the world,” adding that “he who understands it, earns it… he who doesn’t, pays it.” While the concept sounds like something straight out of a complex high school mathematics textbook, it is actually the single most powerful wealth-building engine available to everyday retail investors.

The primary reason many people fail to build long-term wealth isn’t because they don’t earn enough money, or because they lack access to exclusive, secretive Wall Street investments. It is simply because they do not understand how to harness the quiet, exponential power of compounding.

In a world driven by a desire for instant gratification, compounding demands patience. It is a slow financial snowball effect that starts entirely unnoticed, only to explode into massive, life-changing numbers decades down the road. If you want to stop trading your physical time for a paycheck and learn how to make your money work tirelessly for you, you must understand how this mathematical phenomenon operates.

This comprehensive guide breaks down the mechanics of compound interest, explains its vital role in your investment portfolio, and provides a clear blueprint to help you maximize its potential to secure your financial freedom.

Simple Interest vs Compound Interest: Understanding the Mathematical Shift in Wealth Creation

To fully appreciate the magic of compounding, we must first compare it to its traditional counterpart: simple interest. Many beginner investors mistakenly calculate their future investment returns using simple interest logic, which severely distorts their long-term expectations.

What Is Simple Interest?

Simple interest is calculated strictly on your original deposit, known as the principal balance. No matter how long you keep your money in an account, you only ever earn returns on that initial amount.

-

The Equation: Imagine you deposit $10,000 into a hypothetical savings account that pays a flat 10% simple interest rate every year.

-

Year 1: You earn 10% of $10,000, which is $1,000. Your total balance is now $11,000.

-

Year 2: You earn another 10% on your original principal of $10,000, which is another $1,000. Your balance becomes $12,000.

-

Year 10: After a decade, you have earned exactly $1,000 every single year, bringing your total balance to $20,000.

With simple interest, your financial growth is entirely linear. It moves forward in a predictable, straight line, generating the exact same dollar amount year after year.

What Is Compound Interest?

Compound interest completely rewrites this equation. Instead of calculating returns solely on your initial principal, compound interest calculates your returns on your principal plus any interest you have already accumulated. It is quite literally “interest earning interest.”

-

The Equation: Let’s look at that same $10,000 initial deposit, but this time it is placed into an investment account that pays a 10% annual compound interest rate.

-

Year 1: You earn 10% on your $10,000 principal, which is $1,000. Your total balance is $11,000. (At this exact point, simple and compound interest look identical).

-

Year 2: This is where the magic begins. Instead of calculating 10% on your initial $10,000, the system calculates 10% on your new balance of $11,000. Your return for Year 2 jumps to $1,100, bringing your new total balance to $12,100.

-

Year 3: The system calculates 10% on $12,100, earning you $1,210 in returns and bumping your balance to $13,310.

-

Year 10: By the end of Year 10, your balance has accelerated to $25,937—nearly $6,000 more than the simple interest account achieved.

[Simple Interest]: Earns money ONLY on your initial deposit ($10,000) -> Linear Growth

[Compound Interest]: Earns money on your deposit + your past earnings -> Exponential Growth

As the cycle continues, your investment returns grow larger every single year, even if you never add another penny of your own money to the account. The interest you earn behaves like a small financial worker, joining forces with your principal to generate a larger wave of earnings the following year.

The Exponential Growth Curve: Why the Element of Time Matters Far More Than the Size of Your Principal

When you look at the numbers above over a brief 3-year or 5-year window, the difference between simple and compound interest seems relatively minor. A few extra hundred dollars might not feel like a revolutionary financial breakthrough. This visual deception is exactly why many investors give up too early; they look at their portfolio after a couple of years, see slow progress, and assume the strategy isn’t working.

However, the defining characteristic of compound interest is that it operates on an exponential growth curve.

In the initial phase of the curve (the first 5 to 10 years), the line moves forward almost completely flat. Progress feels slow and grueling. But once you cross a specific time horizon threshold, the curve hits its inflection point and bends sharply upward, skyrocketing into near-vertical growth.

The Story of the Two Friends: A Lesson in Starting Early

To see the immense power of time over principal size, let us look at a classic financial case study involving two hypothetical investors: Chris and Jessica. Both earn the exact same average 8% annual compound return on their investments.

Jessica: Starts at age 25 ──► Invests $3,000/year for 10 years ($30,000 total) ──► STOPS completely

Chris: Starts at age 35 ──► Invests $3,000/year for 30 years ($90,000 total) ──► CONTINUES to 65

-

Jessica’s Move: Jessica starts investing at age 25. She deposits $3,000 every single year into a retirement account. She maintains this habit for exactly 10 years, contributing a total of $30,000 of her own money. At age 35, she stops adding money completely and simply leaves her account untouched to compound until she reaches age 65.

-

Chris’s Move: Chris delays his investing journey, waiting until he turns 35 to get started. He invests that exact same $3,000 every single year, but he keeps adding money for 30 years straight until he hits age 65. In total, Chris contributes a staggering $90,000 of his own money—three times more than Jessica.

The Astonishing Final Result at Age 65

When both reach retirement age at 65, who do you think walks away with a larger net worth?

Intuitively, most people assume Chris wins by a landslide because he invested for three times longer and contributed far more cash. However, thanks to the mathematical reality of compound interest, Jessica wins.

-

Jessica’s Final Nest Egg: $314,870

-

Chris’s Final Nest Egg: $309,960

Even though Jessica never contributed another single dollar after her 35th birthday, her ten-year head start allowed her portfolio to build up a massive critical mass of compound interest. That interest continued to multiply completely on autopilot for an extra decade, easily outpacing Chris’s heavy manual contributions.

The takeaway is absolute: time is your greatest asset. Your compounding timeline matters vastly more than the size of your initial bank deposits.

How the Stock Market Compounds Capital Through Reinvested Dividends and Stock Splits

When people learn about the formula for compound interest, they often ask a highly practical question: “How does this actually happen in the stock market? Stocks aren’t a traditional savings account that distributes a fixed monthly interest check.”

In the equities market, compounding is driven primarily by two powerful mechanisms: capital appreciation and Dividend Reinvestment Plans (DRIP).

1. Exponential Capital Appreciation

When you purchase shares of an exchange-traded fund (ETF) or an individual stock, you own a piece of a real business. If that business increases its revenues, scales its infrastructure, and grows its profitability over time, the actual value of your share increases.

If a stock grows at an average rate of 10% per year, it means it is growing relative to its value from the previous year, not its original price from a decade ago. This continuous compounding of the company’s valuation naturally drives your personal net worth upward on an exponential scale.

2. The DRIP Mechanism: The Ultimate Portfolio Accelerant

Many mature, highly profitable blue-chip corporations distribute a portion of their profits directly back to their shareholders in the form of cash payments called dividends. If you receive these dividends as cash deposited into your checking account and spend them on daily lifestyle purchases, you are actively interrupting the compounding process.

To truly tap into compound interest, you must activate a features in your modern brokerage account known as a Dividend Reinvestment Plan (DRIP).

┌────────────────────────────────────────┐

│ Company Pays Cash Dividends │

└───────────────────┬────────────────────┘

│

▼

┌────────────────────────────────────────┐

│ Brokerage Automatically Reinvests │ ──► Buys Fractional Shares

└───────────────────┬────────────────────┘

│

▼

┌────────────────────────────────────────┐

│ You Own More Shares next Quarter │ ──► Generates Even Larger Dividends

└────────────────────────────────────────┘

With DRIP enabled, the moment a corporation pays you a dividend, your brokerage platform automatically uses that cash to purchase more shares (or fractional shares) of that same asset, completely bypassing any manual effort or transaction fees.

The next quarter, because you now own a larger pool of shares, you receive an even larger cash dividend payout, which is used to buy even more shares. This creates a highly efficient compounding feedback loop, converting regular cash flow into a growing avalanche of equity assets.

The Dangerous Flip Side of Compounding: How Fees, Inflation, and High-Interest Debt Can Destroy Your Wealth

While compound interest is the ultimate tool for wealth creation, it is a double-edged sword. The exact same exponential mathematical rules that can turn a modest savings rate into a multi-million dollar portfolio can also be used against you to cause financial ruin. Compounding is entirely blind to whether it is working for your net worth or for a financial corporation’s balance sheet.

1. The Wealth-Destroying Power of Credit Card Debt

The absolute clearest example of compound interest working in reverse is credit card debt. When you carry an outstanding balance on a credit card, the financial institution charges you an annual interest rate that is often compounding on a daily or monthly basis.

Because credit card interest rates are notoriously high—frequently hovering between 18% and 25%—the mathematical snowball effect triggers rapidly against you. If you only pay the absolute minimum statement balance each month, your payments barely scratch the surface of the interest fees. The unpaid interest rolls over into the next cycle, expanding your principal balance and causing your debt to spiral out of control.

2. How Expense Ratios and Fees Silently Drain Your Returns

When choosing mutual funds or ETFs, many retail investors ignore the tiny management fee known as the expense ratio. A fee of 1% or 1.5% might sound completely harmless on paper, but when applied to a compounding portfolio over a 30-year or 40-year investment window, high fees act as a massive parasite that saps your financial growth.

| Investment Framework | Annual Return | Management Fee | True Return | Portfolio Value After 30 Years | Lost to Fees |

| Low-Cost Index Fund | 9.0% | 0.05% | 8.95% | $121,380 | Minimal |

| Active Mutual Fund | 9.0% | 1.50% | 7.50% | $87,540 | $33,840 (28%) |

As the data demonstrates, an investor who deposits a single $10,000 principal into an active mutual fund charging a 1.5% fee ends up losing over 28% of their entire potential future wealth compared to a low-cost index fund. The fee doesn’t just subtract money today; it subtracts money that could have been compounding for you over the next three decades.

3. The Silent Erosion of Cash via Inflation

Inflation is the continuous, steady increase in the price of everyday goods and services, which naturally lowers the purchasing power of your money. If inflation is running at an average of 3% per year, it acts exactly like a negative compound interest rate on any idle cash sitting in a traditional checking account.

Leaving your long-term life savings sitting entirely in cash means your money is actively decaying in value over time. To preserve and scale your purchasing power, you must deploy your capital into compounding market assets that historically outperform the baseline rate of inflation.

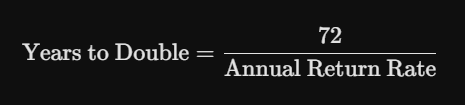

Mathematical Formulas Simplified: The Rule of 72 and How to Project Your Future Net Worth

To navigate your investment strategy effectively, you do not need to memorize complex algebraic equations. Instead, you can rely on a brilliant, time-tested mental shortcut known as The Rule of 72. This rule allows you to estimate exactly how many years it will take for your invested capital to double in value at any given compound return rate.

How to Use the Rule of 72

The formula is incredibly simple. Take the number 72 and divide it by the expected annual interest rate or return rate of your investment portfolio. The resulting number is the approximate number of years required to turn your money into two times its current size.

Let us look at three distinct historical asset return scenarios using this mental model:

-

Scenario A (High-Yield Savings Account): Imagine you place your emergency cash in an account earning a steady 4% annual interest rate. Take 72 divided by 4, and you discover it will take roughly 18 years for your money to double in size.

-

Scenario B (Historical Stock Market Average): Imagine you invest your capital into a diversified S&P 500 index fund, which has historically delivered a long-term average annual return of roughly 8% when adjusted for inflation. Divide 72 by 8, and you learn that your portfolio value will naturally double every 9 years.

-

Scenario C (High-Growth Real Estate/Equities): Imagine you secure a highly optimized, aggressive portfolio that yields an average return of 12% per year. Divide 72 by 12, and your capital doubles every 6 years.

By keeping the Rule of 72 in your financial toolkit, you can quickly project your long-term financial milestones without needing to pull up an advanced online calculator, keeping your wealth goals crystal clear.

Psychological Barriers: Overcoming the Desire for Instant Gratification to Build Real Wealth

If compound interest is purely mechanical and mathematical, why isn’t everyone wealthy? It is because the primary challenges of investing are completely psychological, not intellectual. To let compound interest work its magic, you must learn to conquer human nature and overcome our hardwired bias for instant gratification.

The Problem with Linear Human Brains

Evolutionarily, the human brain is hardwired to think in strictly linear terms. If we take ten steps forward, we intuitively expect to be ten meters away. If we look at our investment portfolio after tracking a disciplined budget for three long years, our linear brains expect to see massive, visual life-altering changes.

When we look at our screen and see that our account balance has only grown from $5,000 to $6,800, we feel a deep sense of disappointment. We think, “I sacrificed my lifestyle, cooked at home, and canceled my subscription services for three years, and all I have to show for it is a measly $1,800 profit? This investing thing isn’t worth the effort.”

Linear Thinking Expectation: Constant, massive visual progress early on.

Actual Compounding Reality: Slow, invisible flat growth followed by an explosive vertical skyrocket.

This psychological letdown is the exact moment where the vast majority of retail investors fail. They abandon their long-term index funds, pull their cash out of the market, and use it to buy a depreciating luxury item or chase a hyper-speculative online trend.

You must understand that the first phase of compound interest is meant to feel boring and unnoticeable. Your job as an investor is to remain emotionally detached from short-term visual feedback, stay consistent with your monthly contributions, and trust the underlying mathematics to handle the heavy lifting over time.

Start Today and Let the Snowball Effect Build Your Fortune

At the end of the day, compound interest is the ultimate financial equalizer. It does not care about your background, your formal education level, or whether you have a massive lump sum of cash ready to deploy right now. It only demands two inputs from you: discipline to start small and patience to let it ride.

| Action Step | Immediate Focus | Long-Term Compounding Result |

| Step 1: Secure the Base | Wipe out high-interest debt and secure an emergency fund | Prevents you from ever needing to interrupt your portfolio growth |

| Step 2: Automate Inflows | Set up recurring monthly deposits into low-cost index funds/ETFs | Ensures continuous asset purchases through all market price points |

| Step 3: Reinvest Everything | Turn on DRIP to automatically reinvest all corporate dividends | Creates an automated, self-sustaining wealth loop that grows over time |

Do not allow analysis paralysis or the fear of a small initial bank balance to keep you sitting on the sidelines of the global economy. Stop waiting for the “perfect financial moment” to begin building your future net worth.

Take immediate action today. Open a low-cost, automated brokerage account, look honestly at your monthly cash flow, identify a modest dollar amount you can easily live without, and configure your system to pay your future self first on autopilot. Stay consistent, ignore the short-term noise of the news headlines, protect your timeline, and watch the unstoppable power of compound interest steadily transform your financial independence into an absolute reality.